The big sector rotation?

Cyclical stocks with catch-up potential

Markets will undergo a reality check in autumn. Following the decline in March, stock markets have risen sharply, and profit expectations for 2021 are high. Even if expansionary monetary and fiscal policies remain the main drivers of rising share prices, much will depend in the short term on whether an effective vaccine is approved this autumn or not. A vaccine would strengthen confidence in the economic recovery and favour a sector rotation from COVID-19 winners to cyclicals.

Patrick Erne

Hopes for a vaccine

Even though we are still in the midst of a raging battle with the COVID-19 crisis, the worst of the global economic slump is behind us. A look at mobility data shows that activity levels in Europe and Asia are already approaching pre-crisis levels. Although Europe experienced a sharper economic downturn than the USA, it is ahead in terms of economic recovery. The rapid approval of a vaccine this autumn is crucial to maintaining current confidence and ensuring economic recovery. Nevertheless, even with vaccination in place, it will take several years before we return to pre-crisis trend growth levels. The number of bankruptcies worldwide will continue to rise, reaching a possible peak in 2021 at the earliest. Consolidation will take place in certain sectors, and highly indebted companies in particular could fall victim to it. Higher unemployment and increasing credit defaults are usually deflationary. However, output capacity in some industries will be at risk of disappearing. If demand for those specific products rises faster and more robustly during the economic recovery, this could then lead to temporary price increases due to capacity bottlenecks.

Ballooning budget deficits and yield curve control

Fiscal policy has become the most important tool for governments during a crisis. The enormous aid packages bring shortterm stability, but the longer-term outlook is rapidly becoming more uncertain. Tackling a debt problem by going even deeper into debt buys you at the most a little more time. In Europe, the main focus is on the possible consequences of redistribution from north to south. In the short term, the eurozone should emerge stronger from this stability pact, and the yield differential between Germany and Italy should narrow in the coming months. In the USA, we are already flirting very heavily with helicopter money since consumers are being supported directly with payments from the government. The current economic crisis is affecting less-qualified workers above all, and the gap between the wealthy and the non-wealthy has widened. There is growing pressure on politicians from voters to convert the stimulus packages – originally intended as temporary aid – into longer-term income support or a guaranteed basic income.

The central banks will be concentrating on controlling the yield curve. The short end of the curve (up to the five-year range) is likely to remain almost unchanged, while the long end should rise slightly as the economy begins to grow again. As long as confidence in monetary policy and government institutions remains high, yields pose little danger. Conversely, this also means that the yield potential of quality bonds has been largely exhausted.

Many healthcare and technology shares were among the beneficiaries of the crisis.

Head of Research

Gold is the most attractive «currency»

Interest-rate differentials between the USD and the other major currencies have narrowed during the crisis. As the economy rebounds, inflation figures will recover over the next 12 months. Real interest rates in most regions will remain deeply embedded in negative territory. Given such an environment, we consider foreign currencies to be less than desirable. In the short term we would prefer the EUR over the USD due to the slightly rosier short-term economic outlook, but upward potential remains limited as no one wants a strong currency. As a result, the fundamental factors are all pointing to further price increases for gold. Investors should not let themselves be rattled by short-term fluctuations in the price of gold due to extreme positions and instead continue to keep physical gold stocks in their vaults.

Cyclical sectors with catch-up potential

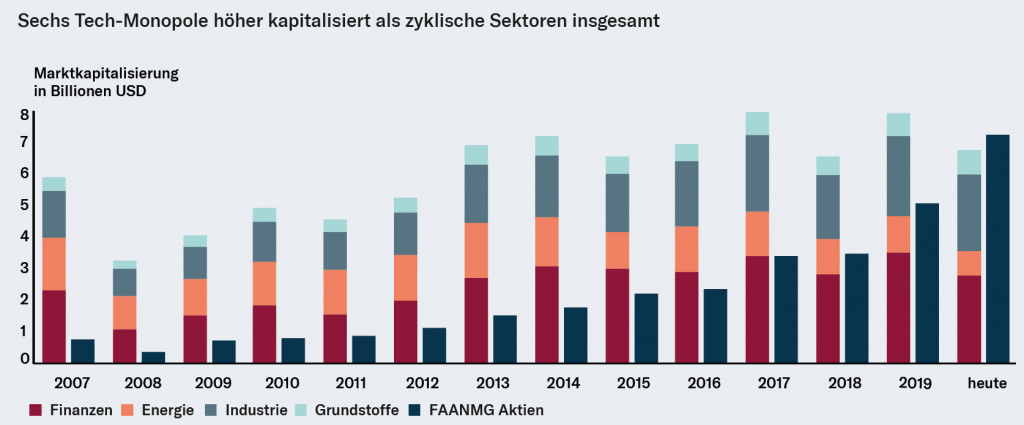

On stock markets, prices for certain sectors and stocks have varied quite significantly during the COVID-19 crisis. Many healthcare and technology shares were among the beneficiaries of the crisis. Due to their high weighting in the indexes, tech stocks are benefiting from an increased cashflow into passive investment vehicles. Cashflow-oriented business models, which have also grown in popularity during the recent economic crisis, continue to favour these stocks. However, some of these companies’ valuations have risen to dizzying heights. And in our view they are too high when compared to the overall market. The market capitalisation of the six major technology stocks (Facebook, Amazon, Apple, Netflix, Microsoft and Google) is currently higher than the total market capitalisation of all of the cyclical sectors in the USA (see chart).

With an economic recovery, a normalisation of inflation expectations, and further stimulus programmes, we foresee improved yield prospects for some cyclical sectors in the coming months. Due to the high weighting of techn shares on the US stock indexes, this could also lead to an underperforming US stock market compared with Europe, at least temporarily. If an effective vaccine is available by autumn, this rotation could gain even more momentum. We therefore recommend that sector allocation should not lean too one-sidedly towards “crisis profiteers” and that cyclical value stocks should be purchased selectively.

Emerging markets benefit from weaker USD

From a structural viewpoint, we have a positive outlook for Asia. However, with the populist-led US election campaign in progress, focus on the rivalry between the USA and China is increasing once again. Nonetheless, the opening up of the Chinese financial market remains a long-standing issue, and its importance on the global equity index will continue to grow. Emerging markets in particular benefit from a weaker USD because many companies and governments hold debt in USD and their debt burden shrinks as a result. We would therefore recommend capitalising on downturns caused by current political discussions to further increase Asian allocation in the long term.

As there is little to suggest a sharp decline in the price of gold based on the low real interest rates and weak USD, we see further potential in gold-mining stocks for risk-oriented investors. Overall, we are positioning ourselves somewhat more cyclically for the third trimester, but without increasing our equity exposure and favouring the European market.